How I Smartened Up My Property Insurance Game — Market-Savvy Tips That Actually Work

You never think about property insurance until you need it — and by then, it’s often too late. I learned this the hard way after a minor storm turned into a major claim headache. That moment pushed me to dig deeper, not just into policy details, but into how market trends shape coverage value. What if your insurance isn’t just protection, but a smart financial move? Let’s explore how forecasting can help you save, protect, and plan smarter — without jargon or fluff.

The Wake-Up Call: When My Roof Leaked and My Policy Failed Me

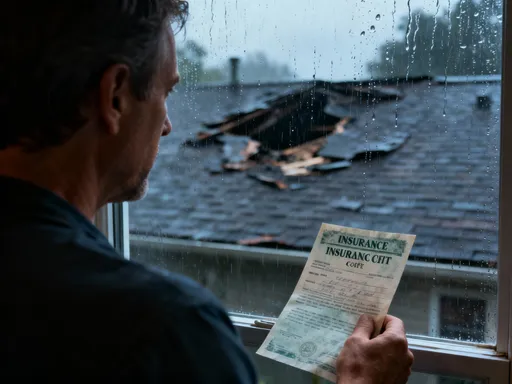

It started with a spring storm — nothing out of the ordinary, or so I thought. Rain lashed against the windows, wind shook the trees, and by morning, water had seeped through a cracked shingle and pooled on my living room ceiling. I called my insurance provider, filed a claim, and expected a smooth repair process. Instead, I received a fraction of what it would cost to fix the damage. The reason? My policy hadn’t kept pace with the rising cost of roofing materials and labor. What I thought was comprehensive coverage turned out to be underinsured, leaving me to cover thousands of dollars out of pocket.

The emotional toll was just as heavy as the financial one. I felt misled, frustrated, and embarrassed. How could I, someone who paid premiums faithfully for years, be so unprepared? I wasn’t alone. Millions of homeowners assume their policies automatically adjust to inflation, market shifts, or home improvements. But most standard policies do not. They’re static — and that rigidity becomes dangerous when economic or environmental conditions change. That storm didn’t just damage my roof; it shattered my trust in a system I’d taken for granted.

This experience became my wake-up call. I realized that treating insurance as a set-it-and-forget-it expense was a mistake. Like any financial decision, it requires attention, review, and strategy. I began researching how market forces influence insurance value, and what I discovered transformed how I view not just property protection, but long-term financial security. Insurance isn’t just about reacting to disasters — it’s about anticipating them.

Beyond the Basics: What Most People Get Wrong About Property Insurance

Many homeowners operate under a few key misconceptions that leave them vulnerable. One common belief is that all property insurance policies are essentially the same — that as long as you have a policy, you’re fully protected. In reality, coverage varies widely between providers and policy types. Some policies exclude certain perils like wind damage, sewer backups, or earthquakes, even in high-risk areas. Others apply broad deductibles that significantly reduce payouts. Assuming your policy covers everything is a gamble few can afford.

Another widespread myth is that premiums are based solely on location. While where you live matters, insurers also consider construction costs, local labor rates, crime statistics, and even the availability of emergency services. For example, two identical homes in neighboring towns might have very different premiums if one is near a fire station and the other is not. More importantly, premiums don’t automatically rise or fall with the actual cost to rebuild your home. If construction prices surge due to supply chain issues or labor shortages, your policy limit may no longer cover replacement costs — even if your premium hasn’t changed.

Inflation is another silent factor that erodes coverage value. Most standard policies do not include automatic inflation adjustment, meaning the $300,000 dwelling coverage you bought ten years ago may only cover 70% of today’s rebuild cost. Yet, many homeowners never reassess their coverage amount unless they’re forced to by a lender or major renovation. This gap between insured value and actual replacement cost is one of the most common reasons for underpayment after a claim. Recognizing these misconceptions is the first step toward smarter insurance planning.

Reading the Market: How Economic Shifts Impact Your Coverage Needs

Property insurance doesn’t exist in a vacuum. It’s deeply influenced by broader economic and environmental trends. When lumber prices spike, rebuild costs go up. When wildfires become more frequent in a region, insurers may raise premiums or impose stricter requirements. When urban infrastructure ages, the risk of water damage from burst pipes or sewer backups increases. These aren’t isolated events — they’re signals that should inform your coverage decisions.

Consider the impact of supply chain disruptions. After the pandemic, the cost of building materials like drywall, roofing, and insulation rose sharply. In some areas, labor shortages doubled wait times for contractors. This means that even a small claim could take months to resolve and cost significantly more than anticipated. If your policy was based on pre-pandemic pricing, you’re likely underinsured. The same applies to areas experiencing rapid real estate appreciation. A home that was worth $250,000 five years ago might now be valued at $400,000 — but if your coverage hasn’t been updated, you’re still insured for the old amount.

Climate trends are also reshaping risk models. Coastal regions face higher wind deductibles and stricter building codes. Areas prone to flooding may see insurers pull out entirely or require separate flood policies. Even inland regions are not immune — increased rainfall has led to more basement flooding in traditionally dry areas. Insurers use sophisticated data to forecast these risks, and homeowners who ignore these shifts are at a disadvantage. Staying informed about local and national trends allows you to anticipate changes before they affect your coverage or premiums.

The Hidden Link Between Property Insurance and Long-Term Wealth Protection

Most people view insurance as a necessary expense — a monthly bill with no immediate return. But this perspective overlooks its role as a wealth preservation tool. Your home is likely your largest asset. Protecting it isn’t just about repairing damage; it’s about safeguarding your financial future. When a claim reveals a coverage gap, the consequences can ripple through your finances for years.

Imagine two homeowners with identical storm damage. One is properly insured and receives a full payout, allowing quick repairs and minimal disruption. The other is underinsured and must take out a loan to cover the difference. That debt accrues interest, delays other financial goals, and may even affect creditworthiness. Over time, the underinsured homeowner loses equity, faces higher stress, and may be forced to sell the home under pressure. Insurance isn’t just about the event — it’s about what happens afterward.

Proper coverage also prevents forced compromises. Without adequate funds, you might choose cheaper materials, delay repairs, or live in unsafe conditions. These shortcuts can reduce your home’s value and increase future risks. On the other hand, a well-structured policy allows you to rebuild to current standards, maintain property value, and avoid financial strain. When viewed this way, insurance isn’t a cost — it’s a strategic investment in stability. It ensures that a single event doesn’t derail decades of financial progress.

Smart Adjustments: Timing Your Policy Changes Like an Investor

Just as investors monitor markets and adjust portfolios, homeowners can time insurance decisions for maximum benefit. The key is knowing when to act. One of the best moments to review coverage is after a home improvement. Adding a new roof, renovating the kitchen, or finishing a basement increases your home’s value — and its rebuild cost. Failing to update your policy means you’re underinsured for the upgraded structure.

Renewal periods are another strategic opportunity. Instead of automatically renewing, use this time to compare quotes, ask about discounts, or negotiate with your current provider. Market competition often leads to better rates, especially when new insurers enter an area. Similarly, if construction material prices are expected to rise — say, due to tariffs or supply constraints — increasing your coverage limit ahead of time can lock in lower rebuild estimates.

Local risk changes also warrant attention. If your area is added to a flood zone, experiences repeated wildfires, or sees a spike in theft, your risk profile shifts. This is the moment to review deductibles, consider additional coverage, or consult an independent agent. Waiting until after a claim is too late. Like an investor who buys high and sells low, a homeowner who waits for disaster to act pays more in the long run. Proactive adjustments, guided by market signals, can save thousands and prevent coverage gaps.

Data-Driven Decisions: Using Public Trends to Forecast Personal Risk

You don’t need to be an economist or meteorologist to make informed insurance choices. Publicly available data can help you assess risk and adjust coverage wisely. Start with FEMA flood maps, which show flood zones and risk levels. Even if you’ve never had water damage, a change in your zone designation could mean you now need flood insurance — or that your lender will require it.

Insurance commissioner reports, published by most states, provide valuable insights into insurer solvency, customer complaints, and claim settlement ratios. These reports can help you evaluate whether your provider is reliable and responsive. If multiple companies are raising rates in your area, it may signal increased risk — a clue to reevaluate your own coverage.

Construction cost indices, such as those from Marshall & Swift or local building departments, track changes in material and labor prices. Reviewing these annually can help you determine if your dwelling coverage is keeping pace. For example, if the index shows a 10% increase in rebuild costs, your policy should reflect that. Some insurers offer guaranteed or extended replacement cost coverage, which provides a buffer against inflation — a valuable feature in volatile markets.

Weather data and climate projections are also useful. The National Oceanic and Atmospheric Administration (NOAA) publishes long-term forecasts and historical storm patterns. If your region is seeing more frequent severe weather, it’s a signal to strengthen your policy. These tools don’t require expertise — just awareness and consistency. Regularly checking these sources turns guesswork into strategy.

Building a Future-Proof Strategy: Flexibility, Review, and Financial Peace

The goal of property insurance isn’t just to survive a disaster — it’s to emerge from it without financial setback. Achieving this requires a mindset shift: from passive policyholder to active risk manager. This means treating your insurance as a dynamic part of your financial plan, not a fixed expense. A future-proof strategy includes regular policy reviews — at least once a year, or after any major life or market change.

Work with insurers or agents who offer flexibility. Some policies allow for automatic inflation adjustments, while others provide options to increase coverage mid-term without penalty. Choose providers with strong claims reputations and transparent terms. If your current insurer resists updates or offers poor customer service, it may be time to switch. Loyalty is valuable, but not at the cost of protection.

Align your coverage with your life stage. A young family in a growing home has different needs than an empty nester planning retirement. As your financial goals evolve, so should your insurance. This holistic approach ensures that your policy supports your broader financial health, not just your roof.

In the end, the peace of mind that comes from being properly insured is priceless. It’s not about fearing disaster — it’s about being ready. It’s knowing that if the worst happens, you won’t face it alone. By understanding market trends, using available data, and making timely adjustments, you turn insurance from a reactive cost into a proactive advantage. These quiet, informed choices don’t make headlines — but they protect everything you’ve worked for. And that’s the true measure of financial wisdom.